Steve H. Hanke: Why Trump’s Wrongheaded Trade Strategy Is A Bust

2019-11-19 IMIPresident Trump repeatedly and proudly proclaims that his trade war strategy and tactics are designed to narrow the trade deficit. But, the facts make it clear that the President’s strategies are not working. Indeed, his assertions have been refuted again and again. Most recently, the U.S. Commerce Department reported that the U.S. trade deficit for both goods and services in the first three quarters of the year jumped by 5.4% over the same period last year. The facts make it clear that Trump’s war plan is wrongheaded—a bust. Yes, Trump is losing his battle to shrink the trade deficit. Why?

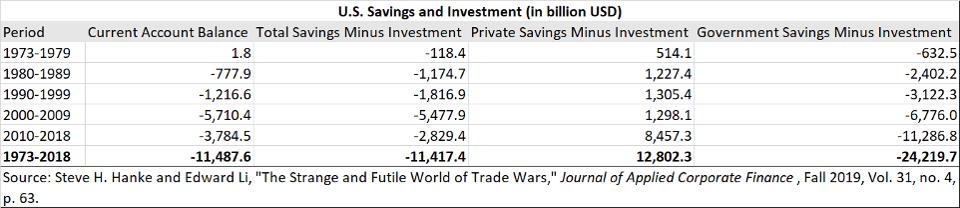

President Trump, alongside many business leaders, has strong views on international trade, particularly the U.S. external balance. He believes an external deficit is a malady caused by foreigners who manipulate exchange rates, impose tariff and non-tariff barriers, steal intellectual property and engage in unfair trade practices. The President and his followers feel the U.S. is victimized by foreigners, as reflected in the country’s negative external balance. This wrongheaded mercantilist view of international trade and external accounts has its roots in how individual businesses operate. A healthy business generates positive free cash flows – revenues exceed outlays. If a business cannot generate positive free cash flows on a sustained basis, take on more debt or issue more equity to finance itself, then it will be forced to declare bankruptcy. Business leaders employ this general free-cash-flow template when they think about the economy and its external balance. For them, a negative external balance for the nation is equivalent to a negative cash flow for a business. In both cases, more cash is going out than is coming in. But, this line of thinking represents a classic fallacy of composition. This is the belief that what is true of a part (a business) is true for the whole (the economy). Alas, economics is littered with fallacies. These cause businessmen to confuse their own arguments about international trade and external balances almost beyond reason. The negative external balance in the U.S. is not a “problem,” nor is it caused by foreigners engaging in nefarious activities. The U.S.’s negative external balance, which the country has registered every year since 1975, is “made in the USA,” a result of its savings deficiency. To view the external balance correctly, the focus should be on the domestic economy. The external balance is homegrown; it is produced by the relationship between domestic savings and domestic investment. Foreigners only come into the picture “through the backdoor.” Countries running external balance deficits must finance them by borrowing from countries running external balance surpluses. It is the gap between a country’s savings and domestic investment that drives and determines its external balance. This is demonstrated by the “savings-investment identity.” In economics, identities play an important role. By definition, they are always true. Identities are derived generally by expressing an aggregate as a sum of parts, or by equating two different breakdowns of a single aggregate. The national savings-investment gap determines the current account balance. Both the public and private sector contribute to the current account balance through their respective savings-investment gaps. The counterpart of the current account balance is the sum of the private savings-investment gap and public savings-investment gap or the public sector balance. The U.S. external deficit, therefore, mirrors what is happening in the U.S. domestic economy. U.S. data support the important savings-investment identity. As shown in the table below, the cumulative current account deficit the U.S. has racked up since 1973 is $11.488 trillion, and the amount by which total savings has fallen short of investment is $11.417 trillion. PROF. STEVE H. HANKE AND EDWARD LI

PROF. STEVE H. HANKE AND EDWARD LI