Xia Le:Prudent Approach to Shadow Banking

2017-06-23 IMI Excessive risk transfer

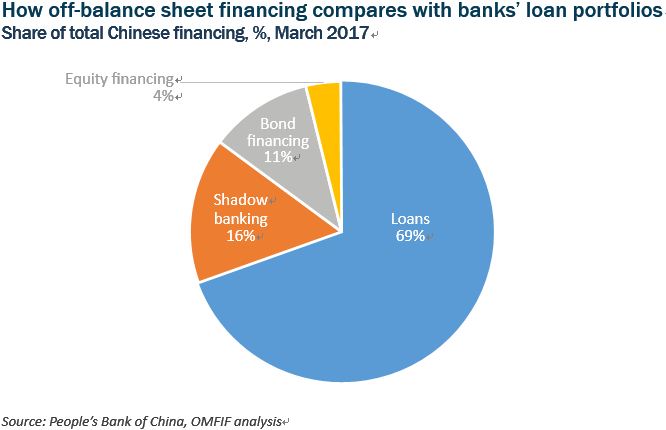

As the bulk of these shadow activities are not reflected on institutions’ balance sheets, existing supervisory requirements of liquidity or capital adequacy cannot effectively limit their expansion. Moreover, the rampant growth of these activities could lead to excessive transfer of risk within the financial sector. Financial institutions may become less incentivised to monitor and manage risks associated with shadow banking, since they believe other parties are taking on those risks through complex deal structures.

Since the start of this year, the volatility of China’s interbank seven-day repo rate (a widely accepted gauge of market interest rates) has significantly increased. Institutions’ reluctance to lend in the money market spilled over to the bond market and raised the financing costs of bond issuance. Up to April, high interest rates led to the delay or cancellation of the issuance of several bonds worth around Rmb260bn.

Furthermore, the liquidity decline is restraining Chinese stock markets. The Shanghai composite index is below the 2016 high recorded in November despite the economy showing stronger than expected momentum in the first four months of 2017.

The shares of small and medium-sized banks and non-banking financial institutions with greater exposure to wealth management products and interbank businesses are under particular pressure.

Coordinated and measured approach

Successfully deleveraging the financial sector while avoiding a systemic debacle is an arduous task. However, a confluence of factors could help the Chinese authorities to do so in a smoother way.

The regulators are paying more attention to communications to avoid unnecessary market upheaval, and authorities are seeking to implement initiatives in a coordinated way. In response to market reactions, they are fine-tuning their pace of regulatory tightening. This measured approach can help them avoid serious policy miscues.

Another buffer the authorities can rely on is the high reserve requirement ratio of China’s banking sector. For large banks, that ratio stands at 17% of total deposits. Even for small and medium-sized banks, the reserve- requirement ratio is 15%. Nonetheless, the authorities can still release a large amount of liquidity to the banking sector when they deem necessary. With such a high reserve- requirement ratio, the authorities have room to manoeuvre along the deleveraging path.

Preserving confidence

Moreover, almost all important Chinese financial institutions are state-owned. That structure might not be good for efficiency, but it could help sustain public confidence in the event of market turmoil. Banks benefit greatly from the ability to take deposits from households and firms during difficult times. The state-owned nature of financial institutions could help to preserve confidence and avert a run on banks.

The deleveraging process may last several years and could be accompanied by heightened volatility in domestic financial markets. There is a risk of declining liquidity and small-scale sell-offs before the authorities achieve their goal.

Although China is exercising tight control of its capital account, the turbulence in domestic financial markets could still spill over to the currency market and put downward pressure on the renminbi.

Worries about a possible renminbi decline could become a key binding constraint for the authorities in pressing ahead with their deleveraging campaign. Regulatory changes may damp the economy by raising funding costs. All this may lead to China experiencing a few years of growth below its potential.

Excessive risk transfer

As the bulk of these shadow activities are not reflected on institutions’ balance sheets, existing supervisory requirements of liquidity or capital adequacy cannot effectively limit their expansion. Moreover, the rampant growth of these activities could lead to excessive transfer of risk within the financial sector. Financial institutions may become less incentivised to monitor and manage risks associated with shadow banking, since they believe other parties are taking on those risks through complex deal structures.

Since the start of this year, the volatility of China’s interbank seven-day repo rate (a widely accepted gauge of market interest rates) has significantly increased. Institutions’ reluctance to lend in the money market spilled over to the bond market and raised the financing costs of bond issuance. Up to April, high interest rates led to the delay or cancellation of the issuance of several bonds worth around Rmb260bn.

Furthermore, the liquidity decline is restraining Chinese stock markets. The Shanghai composite index is below the 2016 high recorded in November despite the economy showing stronger than expected momentum in the first four months of 2017.

The shares of small and medium-sized banks and non-banking financial institutions with greater exposure to wealth management products and interbank businesses are under particular pressure.

Coordinated and measured approach

Successfully deleveraging the financial sector while avoiding a systemic debacle is an arduous task. However, a confluence of factors could help the Chinese authorities to do so in a smoother way.

The regulators are paying more attention to communications to avoid unnecessary market upheaval, and authorities are seeking to implement initiatives in a coordinated way. In response to market reactions, they are fine-tuning their pace of regulatory tightening. This measured approach can help them avoid serious policy miscues.

Another buffer the authorities can rely on is the high reserve requirement ratio of China’s banking sector. For large banks, that ratio stands at 17% of total deposits. Even for small and medium-sized banks, the reserve- requirement ratio is 15%. Nonetheless, the authorities can still release a large amount of liquidity to the banking sector when they deem necessary. With such a high reserve- requirement ratio, the authorities have room to manoeuvre along the deleveraging path.

Preserving confidence

Moreover, almost all important Chinese financial institutions are state-owned. That structure might not be good for efficiency, but it could help sustain public confidence in the event of market turmoil. Banks benefit greatly from the ability to take deposits from households and firms during difficult times. The state-owned nature of financial institutions could help to preserve confidence and avert a run on banks.

The deleveraging process may last several years and could be accompanied by heightened volatility in domestic financial markets. There is a risk of declining liquidity and small-scale sell-offs before the authorities achieve their goal.

Although China is exercising tight control of its capital account, the turbulence in domestic financial markets could still spill over to the currency market and put downward pressure on the renminbi.

Worries about a possible renminbi decline could become a key binding constraint for the authorities in pressing ahead with their deleveraging campaign. Regulatory changes may damp the economy by raising funding costs. All this may lead to China experiencing a few years of growth below its potential.