Steve H. Hanke: Currency Wars, the Devaluation Delusion

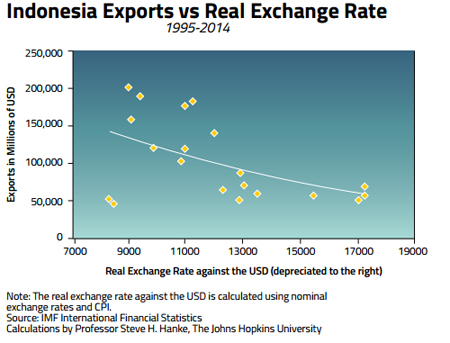

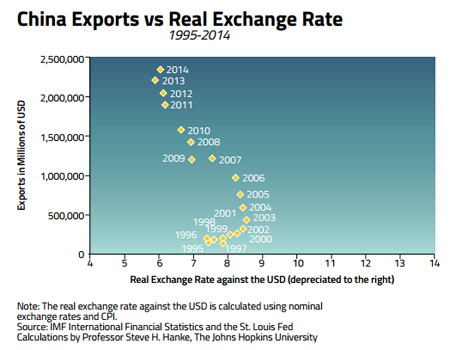

2016-04-08 IMI The case of China, like that of Indonesia’s, runs counter to conventional wisdom. China, from 1995 – 2014, is of particular interest and importance because the RMB is at the center of the so-called currency wars. As the accompanying chart shows, the RMB, in real terms, has mildly appreciated against the greenback, and Chinese exports have soared. These data not only poke a hole in the layman’s notions about the wonders of weak currencies, but also illustrate why most politicians are ignorant of the basic facts, and could be successfully prosecuted for false advertising.

The case of China, like that of Indonesia’s, runs counter to conventional wisdom. China, from 1995 – 2014, is of particular interest and importance because the RMB is at the center of the so-called currency wars. As the accompanying chart shows, the RMB, in real terms, has mildly appreciated against the greenback, and Chinese exports have soared. These data not only poke a hole in the layman’s notions about the wonders of weak currencies, but also illustrate why most politicians are ignorant of the basic facts, and could be successfully prosecuted for false advertising.

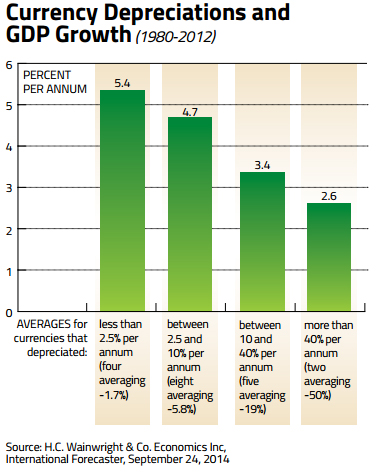

When we move beyond a country’s exports to its GDP, we find the same picture: currency devaluations are associated with slower GDP growth. David Ranson studied the relationship between currency devaluations and GDP growth for nineteen countries in the 1980 – 2012 period. The results are clear: to slow down economic growth, call for a currency devaluation (see the accompanying chart).

When we move beyond a country’s exports to its GDP, we find the same picture: currency devaluations are associated with slower GDP growth. David Ranson studied the relationship between currency devaluations and GDP growth for nineteen countries in the 1980 – 2012 period. The results are clear: to slow down economic growth, call for a currency devaluation (see the accompanying chart).

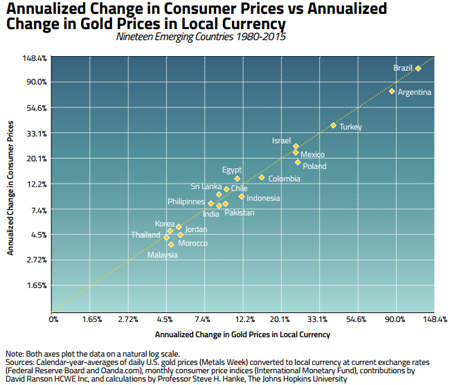

So, if devaluations fail to deliver more trade and higher GDP growth rates, what do they deliver? Well, one thing devaluations deliver is inflation. If we measure the strength of local currencies by the price of gold in those currencies, a virtual one-to-one relationship between the increase in the price of gold in a local currency (a weakening currency value) and a country’s annualized inflation rate exists. The accompanying chart for nineteen developing countries, over the 1980 – 2015 period, shows the tight link between a weaker currency and higher inflation rates.

So, if devaluations fail to deliver more trade and higher GDP growth rates, what do they deliver? Well, one thing devaluations deliver is inflation. If we measure the strength of local currencies by the price of gold in those currencies, a virtual one-to-one relationship between the increase in the price of gold in a local currency (a weakening currency value) and a country’s annualized inflation rate exists. The accompanying chart for nineteen developing countries, over the 1980 – 2015 period, shows the tight link between a weaker currency and higher inflation rates.

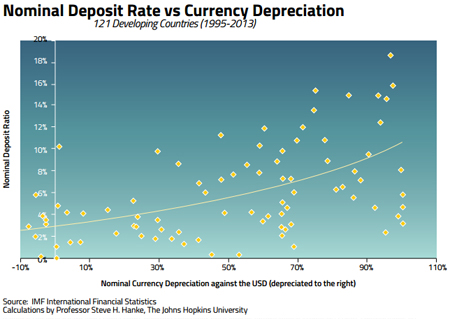

In addition, devaluations deliver higher interest rates, as the accompanying chart illustrates. When developing countries’ currencies are devalued against the U.S. dollar, interest rates in those countries go up. This results because people with assets denominated in currencies that are depreciating demand higher interest rates to compensate for the local currency’s loss in value relative to the U.S. dollar.

In addition, devaluations deliver higher interest rates, as the accompanying chart illustrates. When developing countries’ currencies are devalued against the U.S. dollar, interest rates in those countries go up. This results because people with assets denominated in currencies that are depreciating demand higher interest rates to compensate for the local currency’s loss in value relative to the U.S. dollar.

The arguments supporting currency devaluations are utterly confused and contradictory supported by neither economic theory nor empirical evidence.

david-marshhow-to-avoid-the-new-mediocre-economy-by-investing-more (2)

The arguments supporting currency devaluations are utterly confused and contradictory supported by neither economic theory nor empirical evidence.

david-marshhow-to-avoid-the-new-mediocre-economy-by-investing-more (2)