Ocean resilience means financial resilience

2026-04-21 IMIThe article was first published on OMFIF on April 13th, 2026.

Maud Abdelli is Global Lead WWF Greening Financial Regulation Initiative and Louise Heaps is Global Lead, WWF Sustainable Blue Economy.

Aligning monetary and financial policy with a sustainable blue economy

The global financial system stands at a crossroads. The ocean, valued at an estimated $24tn in assets and generating $2.5tn in annual gross value added, is an essential pillar of macroeconomic stability. Yet, the health of this vast marine capital is under immense pressure from overexploitation, pollution, ecosystem degradation and the impacts of climate change. Its decline represents not only an environmental risk; it is a material macro-financial risk with direct implications for price stability, sovereign creditworthiness and the resilience of our financial system.

As stewards of financial stability, central banks, financial regulators and supervisors have a pivotal role to play in ensuring that the financial system supports, rather than undermines, the ocean’s resilience.

A sustainable blue economy, one that safeguards and restores vulnerable ocean ecosystems while delivering social and economic benefits, requires a fundamental rethinking of how monetary and financial policy account for natural capital.

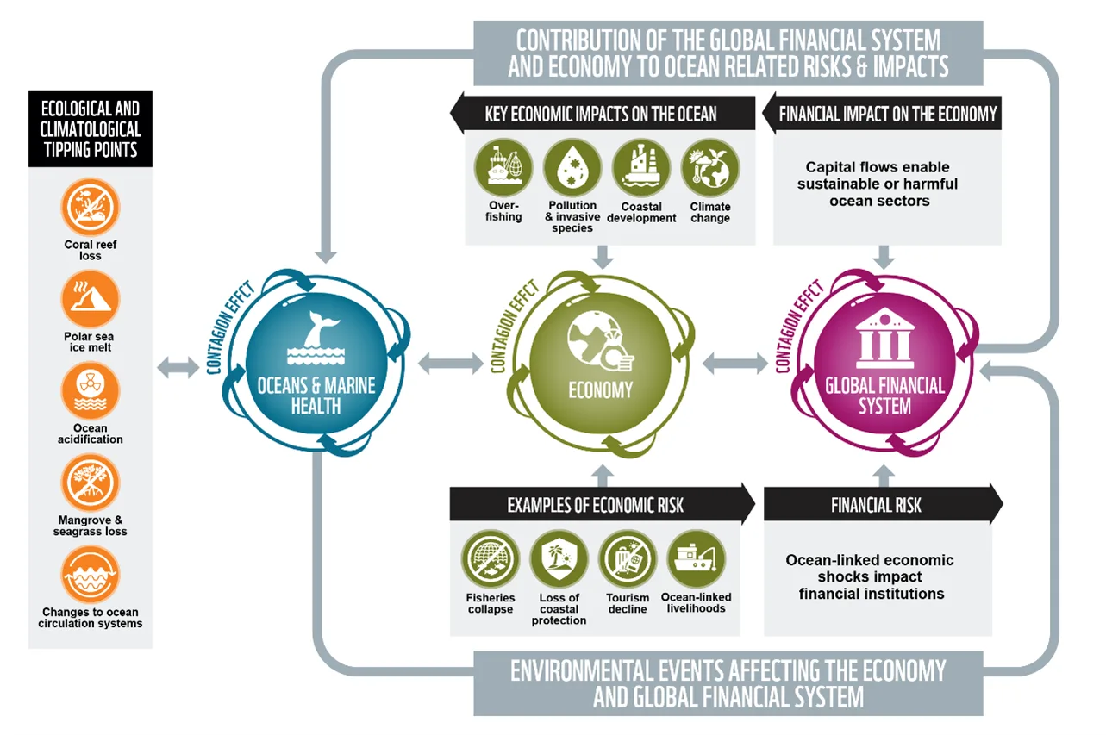

Figure 1. Transmission channels of ocean-related risks to the financial system

Source: Network for Greening the Financial System, Almeida & Reitmeier (2024) and WWF

Today, ocean-related risks and dependencies remain largely unpriced and invisible within financial decision-making. Harmful subsidies, poorly priced marine resources and an absence of ocean-related risk metrics continue to drive unsustainable marine sectors. Various scientific research shows that ocean degradation threatens to accelerate physical climate risks, disrupt global supply chains and increase volatility across financial markets.

Ecosystem tipping points – such as the loss of coral reefs from significant bleaching events or the potential disruption of the Atlantic Meridional Overturning Circulation – are highly likely to trigger abrupt, irreversible shifts with profound macroeconomic consequences. Correcting these distortions will demand a coordinated effort across fiscal, monetary and regulatory areas.

For financial authorities, the imperative is clear: ocean health must be integrated as a core element in financial regulation and monetary policy, and should include a broader governance approach involving fiscal policies.

Financial regulators and central banks are increasingly recognising that climate- and nature-related risks have wide, systemic implications. The same logic applies to the ocean. Embedding ocean-related physical and transition risks into supervisory, macroprudential oversight and scenario stress-testing can enhance resilience across the financial system. This is consistent with the guiding principles of the Network for Greening the Financial System and aligns with global efforts to integrate biodiversity into financial decision-making. Frameworks developed through the NGFS already provide a foundation for incorporating nature-related risks; these can be expanded to include ocean-specific metrics and ecosystem tipping points.

Ocean-related risks can also affect price stability and should therefore be considered in monetary policy. Addressing them presents an opportunity for central banks to better align policy with transition goals while reducing risks to the financial system.

Monetary policy can help channel capital towards ocean-positive investments. Through green and blue refinancing frameworks, central banks could lower the cost of capital by accepting high-quality ocean-positive assets – such as sustainable fisheries, offshore renewable energy or coastal restoration projects – as collateral. Green finance has already proven effective in driving clean energy investment. Applying similar tools to the ocean economy could deliver comparable benefits.

Each year, an estimated $35bn in global subsidies continues to support overfishing, while fossil fuel subsidies distort energy markets and accelerate ocean warming and acidification. Fiscal and public-finance institutions can remove these persistent market distortions. Harmful subsidies – including those supporting fossil fuels and industrial overfishing – continue to drive ocean degradation. Redirecting these funds towards building coastal resilience, including in blue carbon ecosystems, sustainable seafood and coastal development, green/blue energy transition and nature-based solutions would strengthen both ecological and economic stability.

The transition to a sustainable blue economy is not a niche environmental area – it is a core requirement for long-term financial stability. To that end, the development of a blue taxonomy – in line with the EU’s green taxonomy – can provide a clear, credible framework for identifying sustainable ocean-related investments.

Ultimately, achieving a sustainable blue economy demands that the financial system internalises the true value of ocean ecosystems. Monetary and financial regulation policies that properly price risk, reward ecosystem restoration and penalise ocean degradation are essential to closing the gap between what our planet and people need and how markets currently behave. A healthy ocean – and the goods and services it provides – is a vital macroeconomic asset that underpins global prosperity.

Financial regulators and monetary authorities already have powerful tools with which to integrate and manage ocean-related risks and to ensure that the financial system is well aligned with the protection and restoration of ocean ecosystems.

The question is no longer whether the financial system should act, but how quickly it can integrate ocean stewardship into its mandate. The health of the global economy depends on the health of the ocean. The financial system must now rise to meet this reality.