A more fragmented global economy awaits after the Iran war

2026-05-21 IMIThe article was first published on OMFIF on May 15th, 2026.

Dennis Shen is a Lecturer in Finance at the International School of Management and a Member of the Supervisory Board of Visioneers.

Conflict, policy volatility and shifting alliances are redefining the global economic landscape

The war between the US-Israel and Iran marks a shift in the global order. Geopolitics is no longer a distant backdrop but rather a central force shaping economies – and a defining feature of Trump 2.0.

Even if many of the kinetic elements of the conflict may presently be on hold, expectations around stability, risk and policy-making have already been altered in ways that are likely to persist.

Although a ceasefire has been achieved, the more important question concerns what follows. Military conflict is costly, domestic pressures in both the US and Iran restrict the tolerance for continuing escalation and disruptions to trade and energy markets give rise to meaningful incentives for some level of stabilisation.

Yet, the path to any negotiated peace has proven fraught. Talks between Washington and Tehran have reportedly met obstacles amid disagreements over sanctions relief, regional security guarantees and the future scope of Iran’s nuclear programme, while US President Donald Trump has continued publicly threatening renewed military action should negotiations falter.

From Tehran’s perspective, any future arrangement must achieve more than temporary de-escalation. Iran seeks not only a deal, but also sufficient leverage to deter future military action from either the US or Israel. In that sense, its demonstrated willingness to disrupt Gulf economies and close the Strait of Hormuz may ultimately prove a more credible deterrent than the nuclear programme itself ever was.

Even after the war is behind us, longer-run fragilities appear inevitable. Recent diplomatic efforts increasingly resemble targeted confidence-building measures rather than any grand bargain – an outcome consistent with previous episodes of US-Iran diplomacy. Rather than heralding durable peace, the current trajectory points towards a delicate settlement designed to prevent immediate re-escalation while leaving many core tensions unresolved.

Regional fragilities

The war has deepened structural vulnerabilities across the Middle East region. Critical infrastructure – especially in energy production and transport corridors – has been exposed, while existing faultlines such as proxy rivalries and governance weaknesses may have been intensified. The region operates today with a meaningfully higher baseline level of risk. Disruptions are more likely, and their global economic effects more immediate.

Geopolitical alignments are evolving. Traditional alliances are giving way to more fluid and transactional relationships. Regional powers are hedging more actively, balancing ties across competing global actors rather than relying on any single partner such as the US. This reflects not just uncertainties around security guarantees but also the growing economic interdependencies between the region and both western as well as Asian economies.

External powers, meanwhile, are increasingly narrowing their focus to core interests such as energy flows and trade routes. Broader ambitions of regional stabilisation have given way to more selective engagements. The result is a more fragmented and less predictable geopolitical ecosystem, one in which coordination may be restricted and crises may be harder to contain.

Geopolitical risk and a moderating role of markets

One of the core lessons of the Iran war has been the degree to which economic and financial pressures have acted as a moderating force.

Markets have displayed a recurring pattern: sharp reactions to escalation followed by recoveries as rhetoric softens or policy shifts towards de-escalation. The ceasefire itself came following the tightening of financial conditions, meaningful rises in energy prices and mounting political pressure from economic fallout. This has seen a shrewd observation that the US president may be constrained by financial conditions – that sufficiently negative reactions prompt inevitable recalibration.

The market narrative commonly described as ‘TACO’ – shorthand for the perception that ‘Trump Always Chickens Out’ by escalating only to later soften or delay such threats – captures such a dynamic. Economic consequences, whether through financial markets, prices at the pump or electoral pressures, decisively shape policy direction. In this sense, market sell-offs may paradoxically act as a counter-cyclical stabiliser, abetting near-term resilience and placing an informal floor beneath extreme outcomes.

Nevertheless, this should not be overstated. Policy reversals are uneven, and the damage from escalation – lost confidence, deferred investment, weakened international coordination – can linger. Rather than delivering stability, such a dynamic risks entrenching a cycle of disruption followed by partial repair, leaving the global system incrementally more fragile.

The outlook in a more fragmented world

For the global economy, the near-term outlook remains the cautious story of resilience, albeit more contingent today on geopolitical events. The ceasefire provides some degree of near-term relief, even as oil inventories fall at record pace and borrowing rates have meaningfully risen.

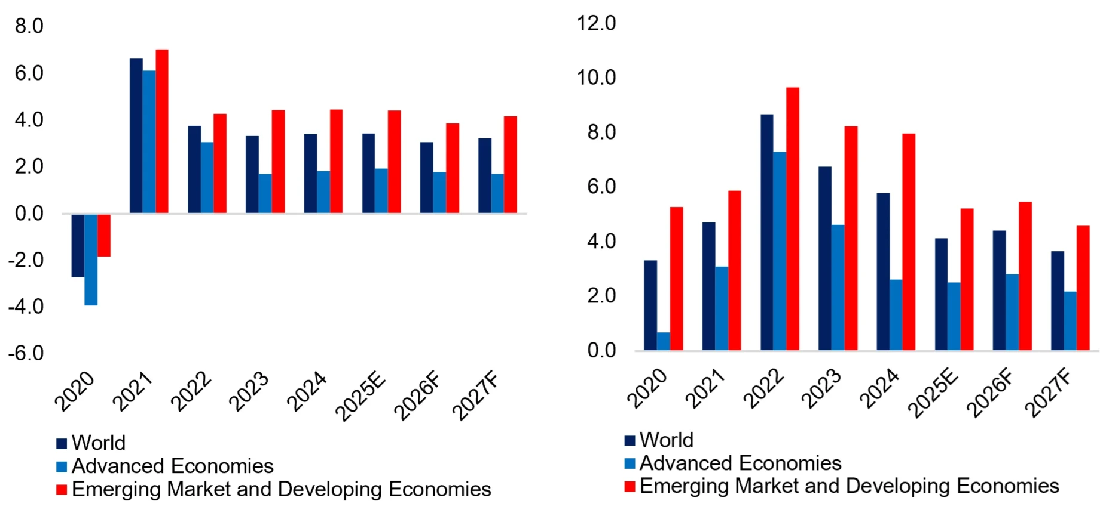

The broader picture has been affected. According to the International Monetary Fund, the war has introduced a drag on global activity. Its latest projections place global growth at 3.1% in 2026 and 3.2% in 2027 – down from recent rates nearer to 3.4%, and below a pre-pandemic historical average of 3.7%. Notably, the 2026 forecast has been revised down by 0.2 percentage points amid heightened geopolitical and commodity-market pressures linked to the conflict. At the same time, global headline inflation is anticipated to rise to 4.4% in 2026 before easing to 3.7% in 2027, reflecting pressures from commodity markets as well as heightened uncertainty (Figure 1).

Figure 1. Global real growth (LHS) and headline inflation (RHS)

%

Source: IMF World Economic Outlook, April 2026

Such figures underscore a salient point: absent the war, the global outlook would most likely have improved. Rather, geopolitical risk is serving as a headwind, offsetting tailwinds from technology investment, supportive policies and rises in equity markets.

The medium-run outlook remains meaningfully more challenging as the economic cycle matures and imbalances build. Elevated geopolitical risks are likely to weigh on investment, especially in exposed regions and sectors. Supply chains may undergo further reconfigurations as firms prioritise resilience over efficiency, raising costs and reducing productivity gains. Inflation may stay elevated, especially if energy markets were to remain sensitive to recurring geopolitical tensions or if significant supply disruptions inevitably re-emerge.

Enduring geopolitical shocks

The war has already accelerated structural shifts underway, such as energy diversification, higher defence spending and the development of alternative trade routes. Such adjustments might strengthen resilience over time, but they also reinforce a broader trend towards global fragmentation and reduced economic integration.

Ultimately, the legacy of the Iran war lies in how it has reshaped expectations. Geopolitical risks are no longer episodic but rather persistent, with policy less predictable and economic stability harder to sustain. The challenge ahead is not simply to recover from this conflict, but rather to adapt to a world within which such shocks are an enduring feature – and where resilience, rather than efficiency, becomes the defining principle of economic strategy.