王卫:房地产企业高信用溢价与严格政府监管间的不匹配

As the capital-intensive industry faces a high level of policy risk, intense market competitions and a high concentration of private-owned enterprises, the sector is crowded with non-investment grade issuers that have to raise funds from the bond market constantly and in large quantities, making them the dominating suppliers in the Chinese HY market.

Their bond funding costs are, on average, higher than that of their peers across the world, and policy causes have also hindered their market access, resulting in higher funding costs offshore than onshore persistently as international investors demand a high risk premium.

There are a number of root causes for the high funding costs issue, including distorted funding access, constraints on HY investor base, and unfavourable credit opinion from international rating agencies.

Yet reality check reveals a mismatch between this high credit premium and the actual credit risk track record, as Chinese property developers had a low default rate and a high recovery rate.

We suggest a number of ways to patch up this market reality gap such as pursuing more transparent and predictable policymaking, broadening international investor base, diversifying funding capacity in both onshore and offshore markets, and enhancing communication with rating agencies.

On the other hand, this market reality gap means Chinese property bonds can offer attractive investment values. Our estimate shows that the high recovery rate of these bonds translates into overpriced credit spread premium in the range of 200bps to 1,000bps for cases with available CDS.

The historical performance of HY Chinese property bonds has also awarded investors handsomely, whether as compared to the stock performance of this sector or to the performance of the US HY bond market.

Although such measures (sometimes a selective combination of the five measures) are mainly aimed at cities experiencing a sizzling housing market, their administrative and interventional nature, sometimes with a surprising element, creates substantial uncertainties and non-market conditions for the industry and the marketplace. As such, they can generate unexpected market imbalances and distortions for both developers and home buyers. In particular, the administrative measures can limit product variety, consumer option, market flexibility and corporate competition, and can also increase business costs, decrease operation efficiency and hurt corporate profitability, which in turn would suppress investor interests and capital resources.

As a basic rule, regulations help to reduce business risks through improving corporate governance, market transparency, financial risk, social sensitivity and price stability, but at the same time push up business costs on increased burdens in operation flexibility, capital efficiency, resource matching, compliance investment and risk taking.

Nevertheless, the motivation behind the governmental regulations is to safeguard the welfare of the broader society. Affordable housing has always been a top priority for policymakers, and containing the financial risk associated with a run-away housing market is also a very important policy target. On the other hand, the real estate industry itself boasts a long value chain and has been a very important pillar for the well-being of the overall economy, employment and tax revenue. So ensuring a stable, healthy and sustainable housing market is critical for both the central and local governments and should be beneficial to the industry itself in the long run.

Their constant need to tap the international bond market has caused some headaches for them along the way. First, the unfriendly government regulations on the industry have put them in a vulnerable position from the beginning, forcing them to seek funds mainly by needs but not much by capital cost efficiency, because in most of the cases, they do not have the option to find the cheapest money in the market or develop the most efficient capital structure for their financial undertaking. That lack of funding flexibility and exposure to regulation vulnerability have artificially degraded their risk profile and thus artificially inflated their funding costs.

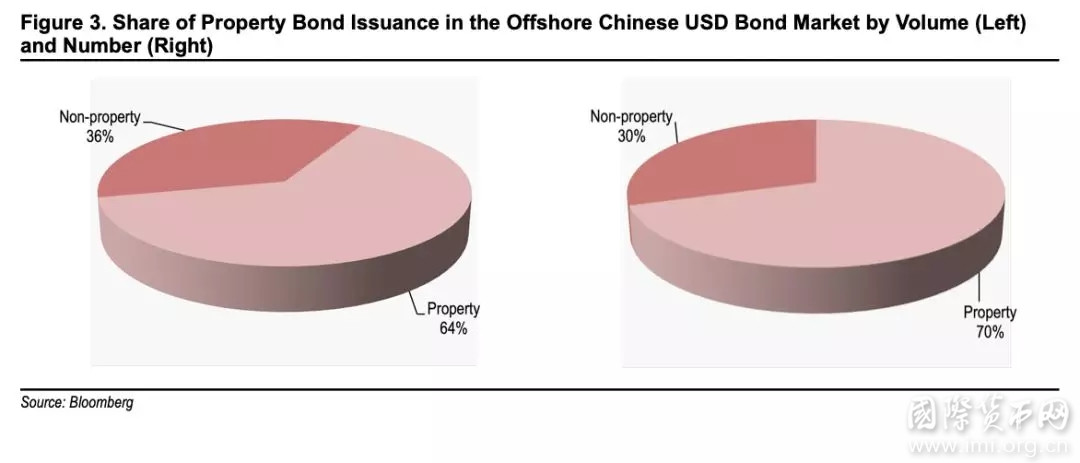

And they get no respite from the international rating agencies, either. The rating opinions from the three international rating agencies (actually at least one from the three) have placed 56 of the total 64 rated developers, or 86%, at non-investment grade ratings (called HY). Figure 3 shows some more details on the Chinese property bonds. Among all the issued Chinese HY bonds in the USD bond market, property bonds have made up 64% in volume and 70% in number since 2009. Obviously, Chinese property bonds dominate the HY sector in the Chinese USD bond market.

The rating agencies’ opinions on Chinese property developers have mainly followed the three major lines of risk concerns. First, they have always considered the current high level of government regulations on the industry as credit negative but not something positive for bond holders; Second, the Chinese developers’ heavy reliance on bond borrowing inevitably results in a high debt leverage, which is a distorted reality due to the governments’ interventions in the market. Third, the majority of the Chinese developers are private-owned enterprises (vs. state-owned enterprises), which are considered a disadvantage from the credit perspective, given the relatively young histories and in many cases, unproven records of these Chinese private-owned enterprises that were only allowed to develop less than 40 years ago. Among the only 9 IG-rated developers, three are privately owned (Vanke, Longfor and Country Garden) while the other 6 are considered SOEs.

What distorts the picture even further is that to make their high-leverage business model sustainable, they have to develop a strong cash flow operation model. Such pressure has resulted in a common practice in the Chinese real estate industry that developers universally adopt a fast turnover operation model so that the fast turnover cycles of their capitals and funds can generate enough return efficiency to compensate their high funding costs. That is why the Chinese residential buildings are called “commodity” homes as they are highly standardised, mass developed and maintain a constant flow of growing supply.

However, such a fast turnover model relies heavily on sustained demands and a merchant-store shopping style practice from the massive Chinese home buyers. Yet the home buyers are also under heavy government regulations and consumer controls, in the forms of various restrictions and limits on their home purchase, mortgage financing, property resale, home refinancing and real estate-related tariffs. The governments’ policy and administrative interventions have created artificial frictions, bottlenecks and barriers on both the supply and demand sides for the Chinese real estate industry and market.

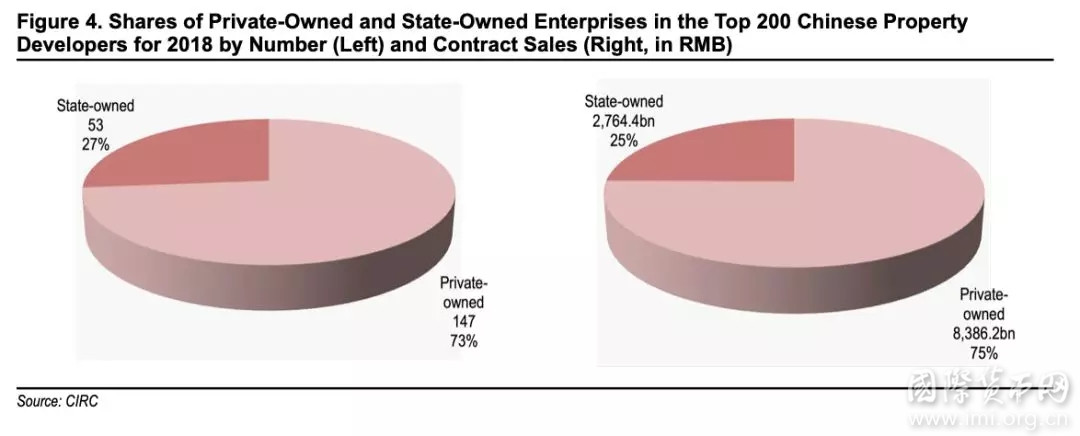

Fortunately, the industry boasts a pride story. The Chinese real estate industry is relatively new and young, with a history of about 35 years since the start of China’s economic reform and opening-up to the world. That was also when private enterprises could enter the industry. And they have flourished over the industry’s young life and become a dominant force in the sector through their relentless efforts of entrepreneurship, competition, innovation and market focus. In fact, as shown in Figure 4, private-owned Chinese property developers made up 73% of Top 200 ranking table issued by CIRC and they contributed 75% of the contract sales among the Top 200 in 2018. While SOEs can benefit from their links to the state to counter balance the negative business environment for their credit strength, those POEs have to absorb all those negativities by their own capacity and resilience, and still come out as industry winners.

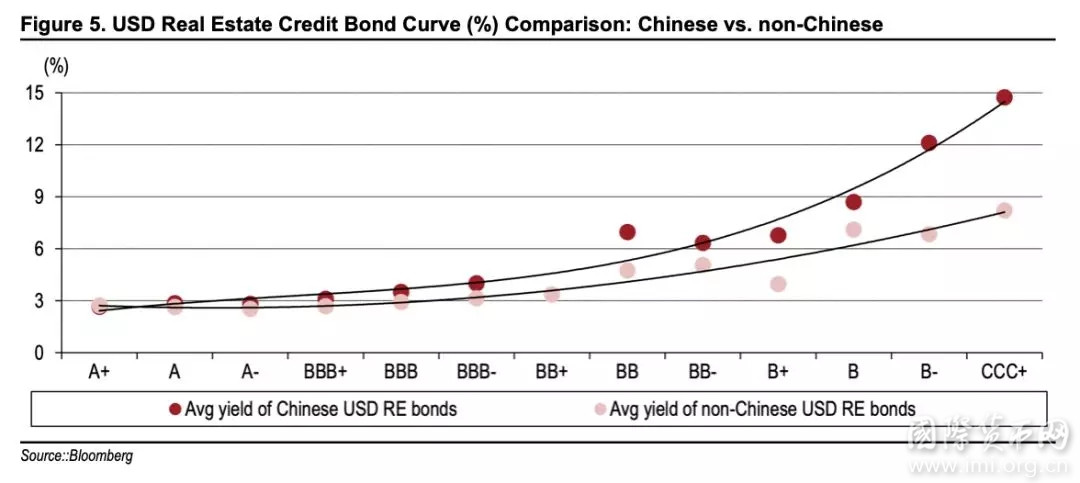

In other words, Chinese RE bonds are perceived by global investors as having relatively much higher risk and thus they demand for a higher risk premium. And we think this risk premium can be attributed to two factors. One is that the fast growing and sometimes overheated Chinese RE market has been under periodic policy tightening pressure, and such policy disruption and intervention elevate risks associated with business and financial uncertainties. The other is a technical factor as the Chinese HY market is dominated by RE bonds and the supply of these bonds has been expanding fast over recent years (as discussed earlier). The ever expanding bond supply places a supply risk premium on this bond sector to reflect investors’ limited capacity of investing in Chinese HY bonds overall and in Chinese HY property bonds in specific. In all, this phenomenon from the Chinese HY property bonds again illustrates a long observed reality that international investors continue to demand a significant valuation discount (yield premium) on Chinese risk assets, including credit products such as property bonds, which we called “China Discount”. The “China Discount” is also reflecting the rating agencies’ risk division that China is considered an EM economy with a non-free market system.

So, it appears that on average, Chinese property developers enjoy a lower bond funding yield in the onshore market than in the offshore market. This can be further illustrated in Figure 7. Here we swap the USD funding cost curve for Chinese RE bonds shown in Figure 3 into equivalent CNY funding cost curve (using cross-currency swap model and assuming an average 3-year tenor for each of the rating categories). The estimated equivalent CNY bond funding cost curve has a yield range of 3.5%-16%, which seems to be higher than the onshore curve range of 4%-8%. In addition, the offshore funding cost curve is also much steeper, again demonstrating the added burden of the HY Chinese property developers that make up the majority of the industry.

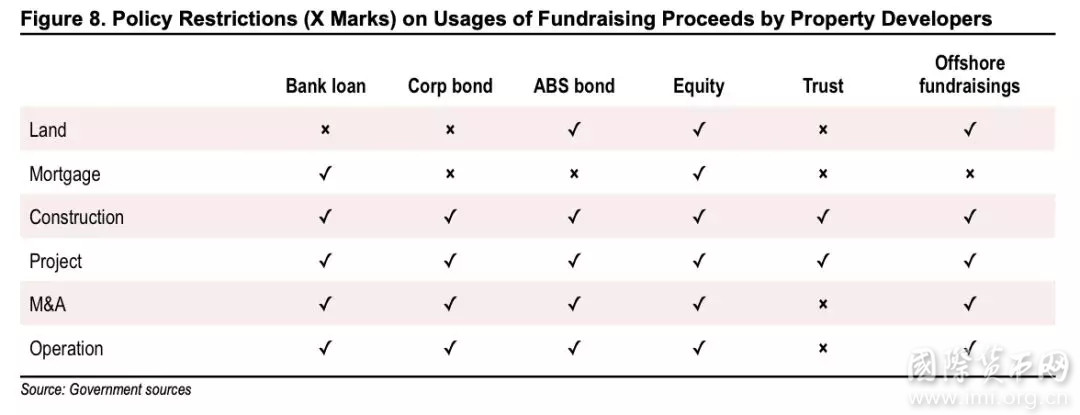

First of all, the market access barrier is the biggest burden for the Chinese property developers. The policy prohibits domestic bond proceeds to be used as capitals for land purchase, M&As or refinancing bank loans. Such restrictions have forced many developers to borrow funds in the international market for their capital needs. This is one of the reasons that more and more Chinese developers came to the offshore bond market for fundraising, which creates crowded supplies from this space and HY supply in particular. The high supply naturally jacks up the funding costs for their borrowings offshore.

To make things worse, offshore borrowings of Chinese firms are in general considered junior to their onshore borrowings due to offshore corporate structure design, cross-border capital control and closeness to corporate assets. Furthermore, their high funding costs in the offshore market could in turn influence the cost pricing of their onshore fundraising, further compounding the financing burden of these firms.

In addition, Chinese firms still need to secure nods from their relevant regulators for their bond issuance in both the onshore and offshore markets, and presently Chinese property developers are facing even more restrictive conditions for seeking regulators’ approvals. Such burdensome restrictions not only reduce the funding flexibility and even market access from the developers, but also create a wide range of business and finance uncertainties, which would both erode investor interests/confidence and result in lost opportunities. Those burdens would eventually translate into added credit costs.

2. HY investor base constraints

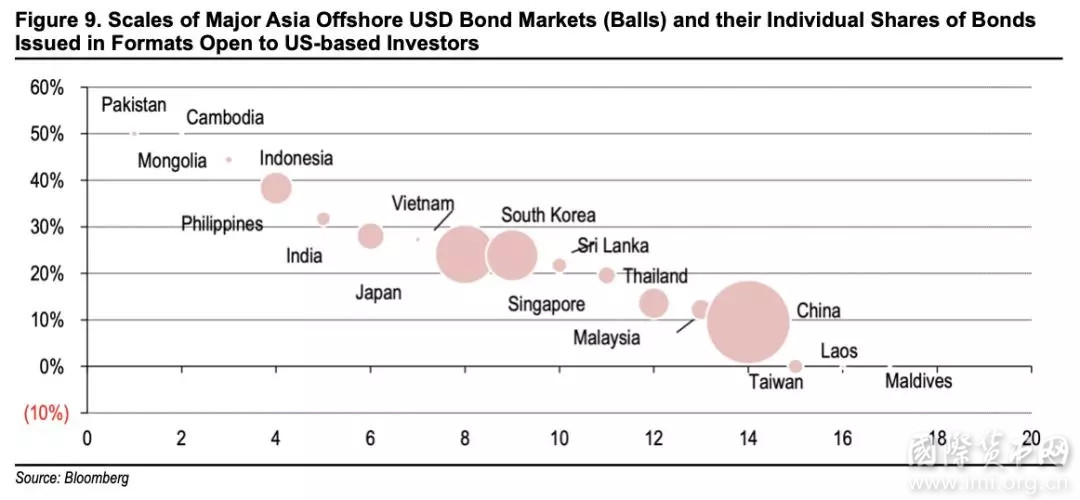

Although bond issuance from Chinese property developers in the international market has been expanding rapidly in recent years, the international investor base for such Chinese investment asset has not been expanding quickly. Currently, over 95% of the HY Chinese bonds were purchased by Asia-based investors and normally only a small percentage went to investors outside the Asian region. In fact, this contrasts sharply to situation that HY bonds from other Asian issuers tend to attract much more non-Asian investors.

Figure 9 shows an example. In the biggest offshore bond market for Chinese borrowers, i.e., the USD bond market, the Chinese issuance eligible to be sold directly to US-based investors makes up a very low percentage of the total, which means the majority of these Chinese USD bonds were sold locally to Asia-based investors. In comparison, USD bond issuers from other major markets such as Japan, South Korea, Indonesia and Malaysia all have higher percentage of participations from US-based investors.

3. Unfavourable rating opinion from international rating agencies

As we discussed earlier, private-owned property developers are the main force in the Chinese real estate industry, but they are mostly rated to the HY space by the three main international rating agencies, in contrast to the fact that those state-owned developers are likely to be rated into the IG space. The rationale remains to be that state-owned Chinese firms enjoy implied government support and are under better governance in additional to their financial fundamentals.

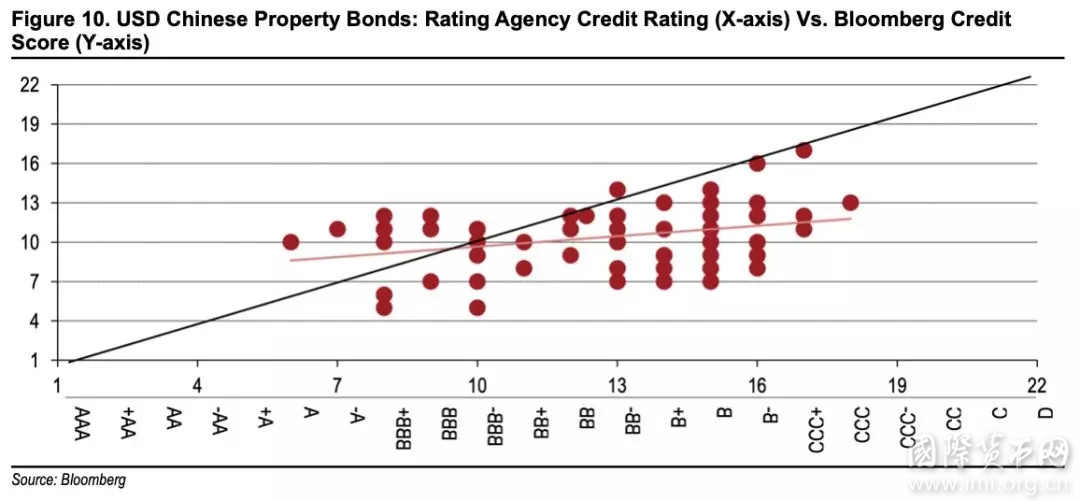

We try to quantify such rating deviations between the agency rating opinion and a fundamentals-based rating score. For a bond with more than one rating from the three main rating agencies, we use the lowest one as the bond’s composite rating representation. On the other hand, we use Bloomberg’s credit default score as a quantitatively estimated credit quality. The Bloomberg credit score measures the default probability of a company over a 1-year horizon, based on both the company’s fundamental financial strengths and its financial market performance.

In theory, both rating methodologies aimed to project the default probability of a credit entity, but their model results can be quite different (see Fig. 10). Their relationship deviates significantly from the diagonal line that represents equal credit score from the two methodologies. In details, their relationship appears to be biased in different directions between the IG and HY segments. In the IG part, the rating agencies tend to give a higher score for credit quality than the Bloomberg quantitative rating suggests, which we think is likely attributed to the fact that the rating agency model gives a considerable weight to the state-ownership factor, as most of the Chinese IG credits, including property developers, are SOEs. Yet, the Bloomberg quantitative credit model does not factor in such a consideration.

However, in the HY part, the rating agencies tend to give a lower credit quality score than the Bloomberg quantitative rating model suggests (tilting toward below the diagonal line). Since nearly all of the HY rated Chinese property developers are private-owned enterprises, they are thus lack of the implied state supportive factor in the agency model.

In our opinion, the Chinese real estate industry is a highly competitive and open-market sector, and the implied significance of the state-ownership has diminished under the current tightening policy from the government. We see no preferential treatments by any levels of government to state-owned property firms to avoid conflicts with the current policy goals.

Despite the highly tough policy environment and intense market competition, Chinese property developers have demonstrated rather admirable credit resilience.

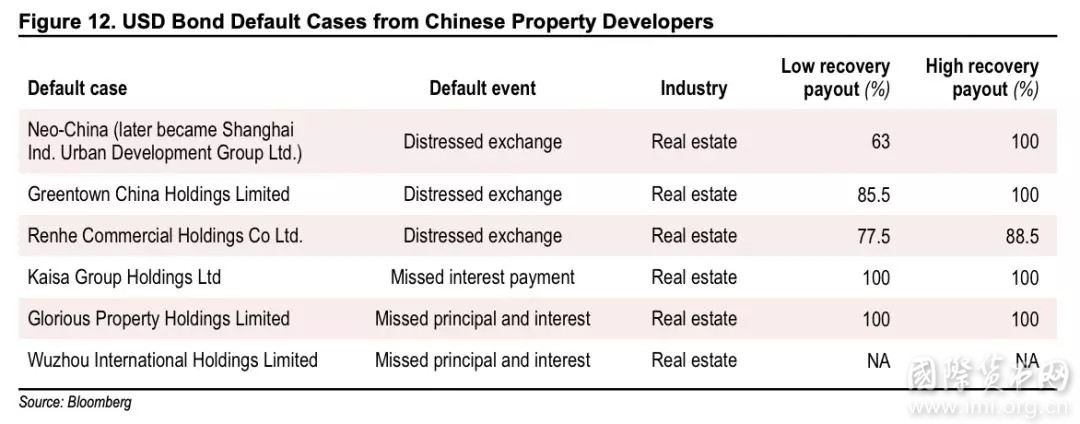

Chinese real estate companies have achieved a quite low default rate over its relatively young history. Among the 76 Chinese real estate firms issuing bonds in the international market, there have only been 6 defaulted issuers so far since 2009, when Neo-China became the first default case from a Chinese property developer in the international bond market (Neo-China was later acquired by a regional SOE - Shanghai Industrial Urban Development Group). That is about 8% rate by issuer count over a 10-year period or a 0.8% annual average.

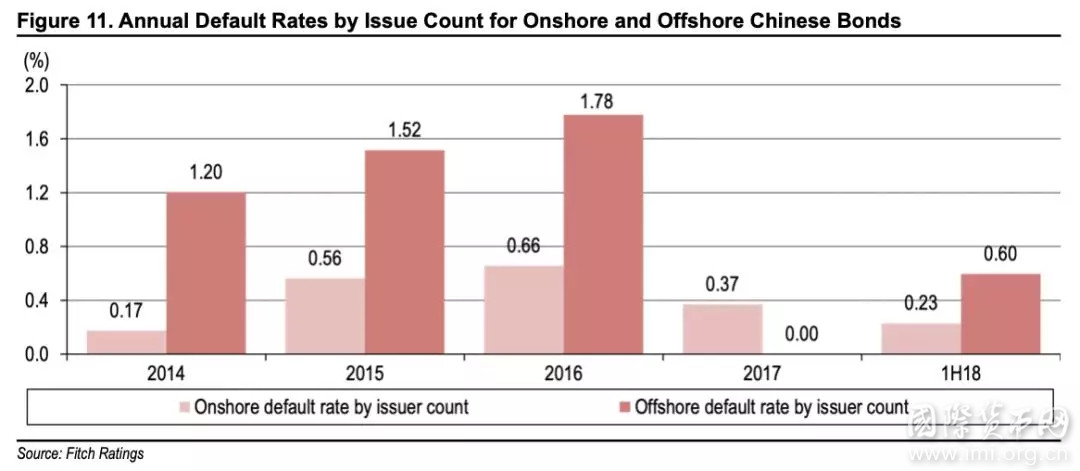

Figure 11 shows Fitch’s estimates of default rates for Chinese bonds over the past 5 years in both the onshore and offshore markets. The onshore annual default rate was in the range of 0.17% - 0.66%, and the offshore rate was in the range of 0% - 1.78%. In comparison, over the same period of time, the estimated annual default rate by Moody’s was in the range of 2.5% - 5% globally and 1.5% - 7.5% for Asia-Pacific. In summary, historically, Chinese bonds in general and Chinese property bonds in particular have incurred much lower default rates for bond investors.

In comparison, the 10-year global corporate average cumulative default rate is about 10% for all rated bonds and 25% for all HY bonds, according to Moody’s.

2. High recovery rate

While Chinese property bonds have demonstrated a better experience in the default front, they have also provided investors with a high recovery rate after defaults. Among the six default cases in the past, none of them had to go to the extreme of corporate liquidations. For the 5 cases with resolutions, all were restructured or settled successfully outside of court, through tender offering, debt swap or eventual full repayment, on high recovery rates (see Fig. 12).

For those resolved cases, the lowest recovery rate was 63.5%, and the highest was 100% in some cases. Again, we found that the Chinese borrowers facing defaults have always exhibited strong will of making the best efforts to repay defaulted interests or principle. On the other hand, the high level of value-holding nature of real estate assets, particularly the rarity of commercial land parcels, also makes it possible for the Chinese developers to raise cash quickly through reselling such hard assets.

In fact, policymakers bear the public duties and power to regulate and supervise the real estate industry for ensuring a stable and affordable housing market, but the credibility and durability of such policymaking is critical for the healthy and sustainable development of the industry so that the market do not have to be burdened by large swings and disruptions. A basic element of good policymaking builds on sufficient public communications, consultations and disclosures before official policy rolls out. Minimising and avoiding the surprising element of policymaking can boost both industry and consumer confidence and benefit risk management. Policymakers also need to carry out the best practices in implementing new policies and regulations so that distorted and imbalanced effects on a key industry and market can be minimised and even avoided.

Given the restrictive nature of the current government policy towards the real estate industry, we try to come out with an estimate on the added financing costs from such tightening policies. Such extra costs due to government policies can be assessed from two angles. One is that Chinese property bonds have to pay higher yields than non-property bonds in both onshore and offshore bond markets. Another is property developers have to pay higher yield in the offshore bond market than in the onshore bond market.

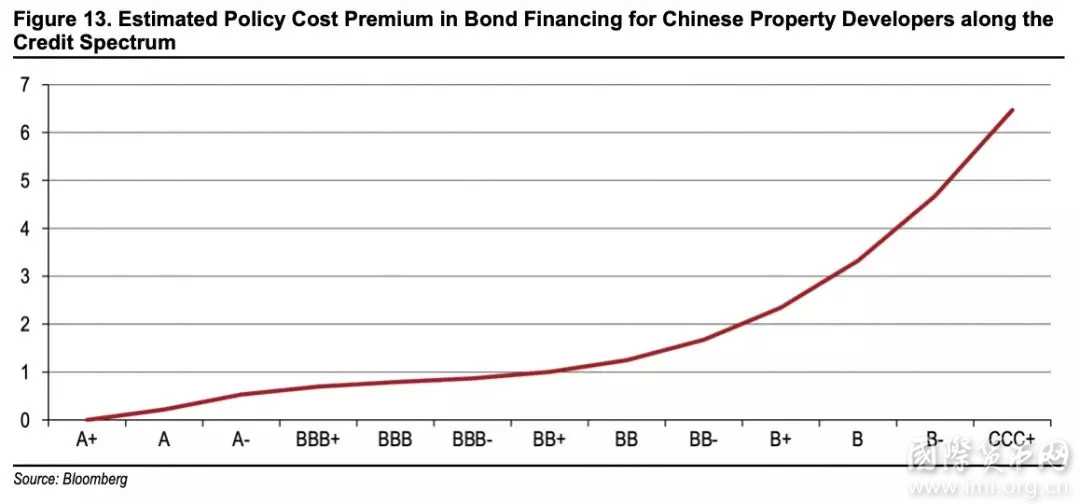

Figure 13 shows the added costs from the first angle, i.e., being a property developer. Basically, we calculate the curve spread between the Chinese property bonds and the Chinese non-property bonds in the USD market, as shown in Fig. 3. The cost premium for property developers is within the level of 100bps for IG bonds, but rises fast over the HY part of the curve (from 100bps at BB+ to 650bps at CCC+). As we discussed earlier, this cost premium for property developers is likely a result of tight government policy towards the sector, forced borrowings in the offshore bond market and biased market risk appetite on the industry, both of the latter two also have a lot to do with government policies.

Additional cost also comes from the yield difference between the onshore and offshore bond markets. There is no direct comparison between onshore and offshore bond markets, because they use different rating systems (local ratings vs. international ratings). Following some practices in the market, we consider locally AAA rated bonds as closely corresponding to investment-grade bonds by international rating scale, and anything below AAA as HY bonds accordingly. We estimated that the AAA rated onshore property bonds have an average USD yield of 4.16%, which is about the same as the 4.06% average yield of the offshore USD bonds (after swapping into CNY equivalent yield). The onshore AAA-rated yield could become even more comparable to the offshore IG yield when considering many of the HY rated issuers in the offshore market have actually been rated in the AAA category.

In the HY space, the average yield of the local property bonds (rated below AAA) is about 6.58%, which is well below the 10.09% average HY yield of offshore bonds (CNY-equivalent yield). Again, we can see that the Chinese property developers, particularly in the HY space, have to pay a much higher bond yield in the offshore market than in the onshore market. If they have a free choice between the two markets without administrative restrictions and limitations, they could have saved significantly in their financial expenses that potentially could help lower the housing prices for home buyers.

2. Broaden international investor base

We have witnessed over the past 10 years or so that Asia has become a very important funding hub for global capital markets. This development is built on the fast-rising wealth from the Asian countries, particularly from the second largest economy of China and maturing financial markets in the region with much more product offerings and greatly expanding market participants. This trend has created for Asia a new global financial centre that can rival with the old-guards of the US and European financial centres. One of the clear outcomes from this development is that most of the Chinese USD bond deals, which now make up about 67% (including HK and Macao, see Fig. 14) of the Asia ex-Japan USD bond market, were done in the Reg-S format, meaning deals are not intended to be sold into the US market. In fact, those deals had very limited participations from European accounts, thus making Asian investors almost the sole driver for the success of those deals.

However, such practices may have some unintended consequences. One of them is that, with exclusion of the US market from most of the Chinese deals, many of the US-based investors find not much incentive to allocate sufficient resources for this market, unless opening a dedicated office in the Asia region to focus on this market. The lack of sufficient research and engagement in this market can only create insufficient understanding, which ultimately can bring risk aversion from these investors in their investment decision on this Asian asset. For the Chinese USD bond market, the continuing lack of significant participation from US-base could constrain rapid growth of the market and miss the important contributions from a large pool of skilled and experienced US portfolio managers for the further maturing up of Chinese credit market.

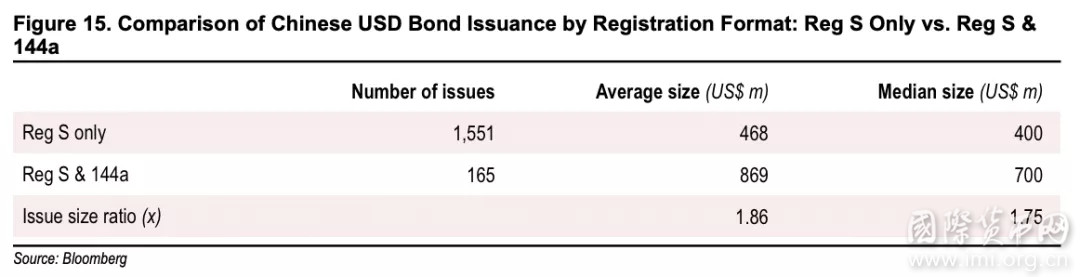

Our analysis on all the Chinese USD issues from the past (including those from HK and Macau, but ignoring deals with size less than US$100m that are most likely privately structured notes) shows one key advantage to include the US market investors (formatted as Reg S & 144a) in a bond deal (see Fig. 15). It shows the Reg S/144a deals got done in much larger issuance size in general (1.86 times by average measure and 1.75 times by median measure). However, we have not found obvious evidence that Reg S/144a formatted deals would enjoy any price advantage at this point.

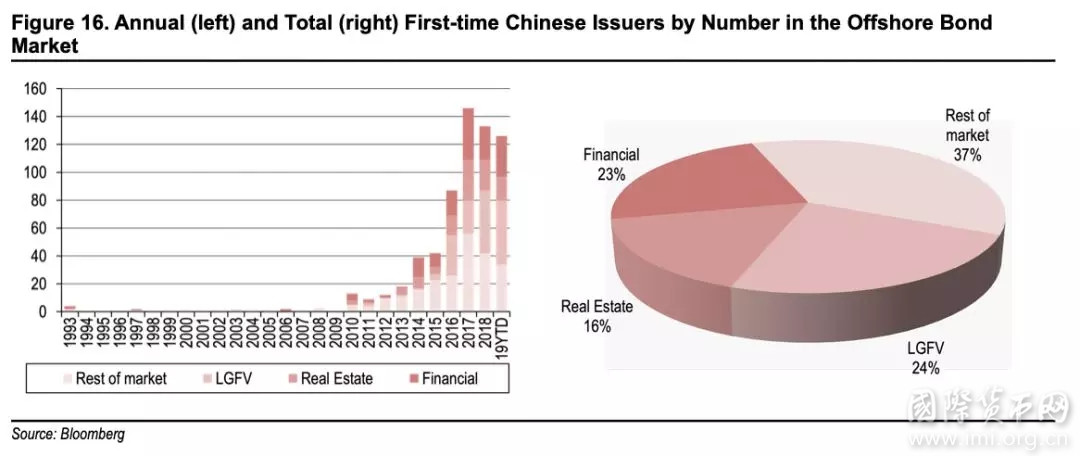

Two sectors have been leading the charge to the scene of the offshore bond market in recent years, in addition to the traditional leader of financial industry. Among them, the LGFV sector has seen the fastest expansion into the overseas bond market since 2014 and the other is the real estate industry. They have made up 24% and 16% of the total new entrances, respectively, as comparing to the 23% share from the big financial industry and 37% from all of the other industry sectors. It is not surprising to see the surging entrance from these two sectors, as they have been facing a continuing unfavourable financing condition at home under government tightening policies. The open and free-market nature of the international capital market puts everyone in an equal footing and level playing field in front of investors’ decision making process, regardless of the background of issuers, such as listed vs. non-listed, state-owned or private-owned, large vs. small, national vs. regional, established vs. new entrants, etc.

4. Enhance communication with rating agencies

Given the dominance of the three major international rating agencies in the global bond market, maintaining effective, consistent and continuous communication with them by Chinese bond issuers remains vital and necessary. Enhancing rating agency communication not only serves as an important part of sound corporate governance practices in corporate disclosure and transparency for the investment public, but also contributes to enhanced dialogues with the rating agencies for their complete, timely and accurate understanding of corporate developments, so that gaps from misunderstanding and misses of important factors in their credit assessment can be minimised or avoided. By doing so, the rating agencies could ultimately help to present a more responsible image for their rating clients.

On the other hand, the continuing efforts from market participants in further promoting and expanding diversity and competing in the rating industry remain very important for a healthy and fair rating market environment. This is not only limited to promoting more competitions among the three major international rating agencies, but also including promoting participations from other rating organisations, such as Chinese rating agencies in the international market.

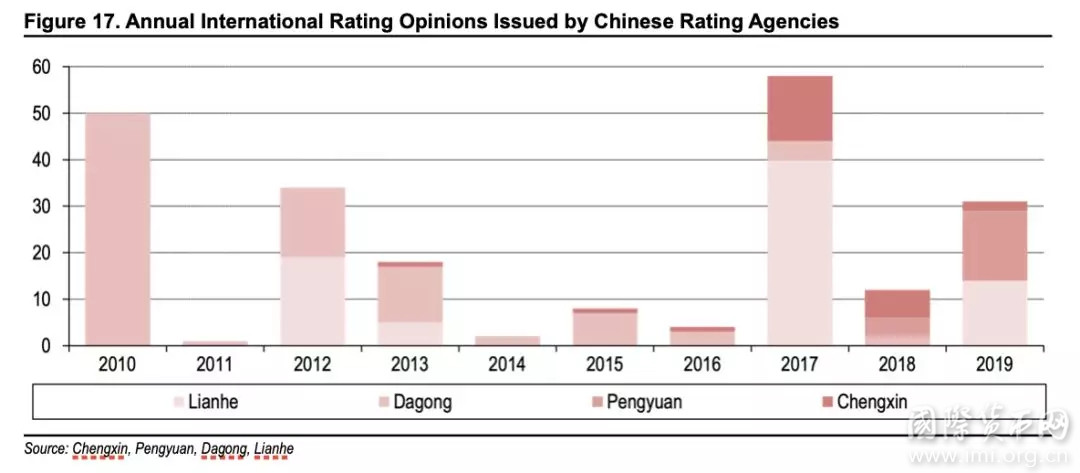

Chinese domestic rating agencies have significantly expanded their business to the international rating market in recent years. A number of them have started to offer credit ratings and opinions on offshore Chinese bond issuers (see Fig. 17). Dagong and Lianhe were two early starters with their focuses on sovereign rating at the early stage, such as Dagong in 2010-2013 and Lianhe in 2012-2017. Over the past 2-3 years, the Chinese rating agencies have been more focused on corporate credit ratings. In addition, Pengyuan has just started to offer offshore ratings for Chinese provincial governments.

The expansion of Chinese rating agencies into the international bond market is positive and timely to the interests of bond borrowers and investors, as the pools of both Chinese issuers and Chinese investors participating in the international bond market continue to grow fast. On the other hand, we also continue to witness an ever increasing number of international investors were attracted to Chinese bonds. The rating opinions from the Chinese rating agencies surely provide another dimension of information and interpretation on the Chinese credits.

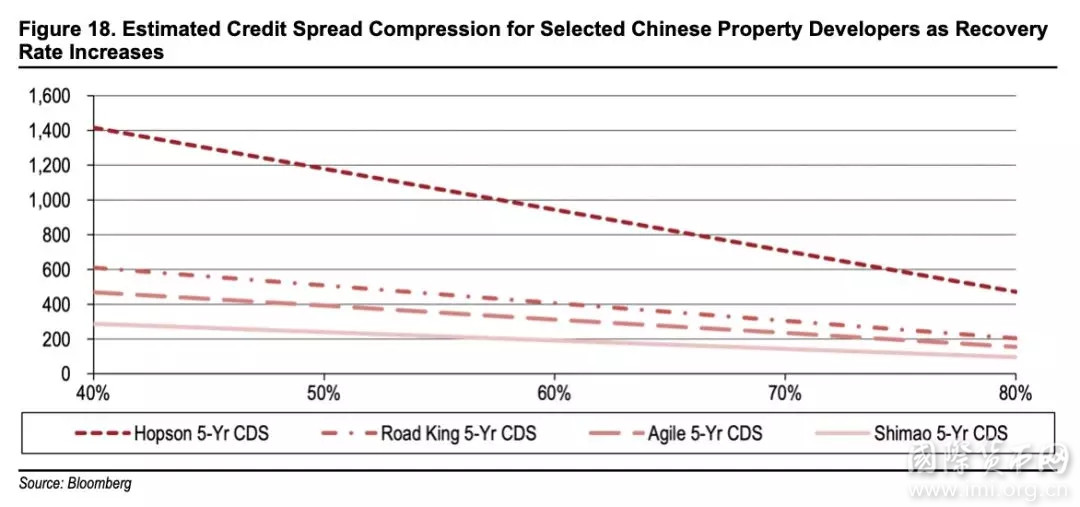

We take the cases at the two ends as examples. In the Hopson case, the CDS spread can narrow down by nearly 950bps when the recovery rate improves from 40% to 80%. In the Shimao case, the reduction is about 190bps. Apparently, both cases demonstrate a very significant credit spread compression from the recovery-rate adjusted CDS pricing.

We believe Chinese property developers have the capacity to maintain such a unique nature of offering high default recovery rates. This unique nature is probably rooted in the Chinese land ownership system that all lands are state owned and land supplies for commercialised development are under strict oversight and control by the government (mainly through an auction-based system), to ensure no mis-selling of state assets and no disruptions to the land market that has been the bread and butter for local fiscal revenues. In other words, being the main hard assets for any Chinese property developer, leased lands from the government and buildings constructed on such lands have been in a perpetual limit of supply in the relatively young history of the Chinese real estate market, and we have all the reasons to believe this state will continue in the foreseeable future.

2. Ample returns for investors

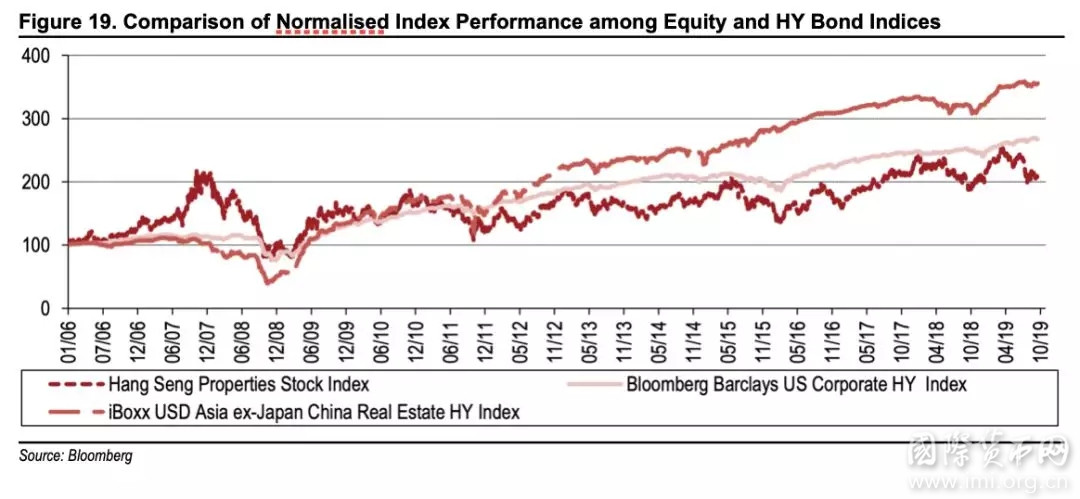

The Chinese USD property bonds have rewarded investors generously since becoming active in the USD bond in 2006. Using index performance as an indicator (see Fig. 19), we can find that iBoxx USD Asia ex-Japan China Real Estate HY Index has outperformed both the Hong Kong Hang Seng Properties Stock Index and the Bloomberg Barclays US Corporate HY Bond Index by a large margin. Over the period since 2006, Chinese bonds have rewarded investors with a 350% index gain, as comparing to the 208% index gain from the Hang Seng properties stocks and 268% index gain from the US HY bonds (we set the first data point of 3 January 2006 as 100).

However, the Chinese HY property bonds appear to be somewhat more volatile than the US HY bonds in general, but the volatility has been down in recent years, making the Chinese HY property bonds even more appealing.